Does Dental Insurance Cover Crowns in Schaumburg?

When a tooth is cracked, heavily decayed, or weakened by a massive old filling, a custom-fitted dental crown is often the most reliable way to save it from extraction. While the immediate priority is always protecting your health and preventing the loss of your natural tooth structure, it is completely normal for your very next thought to be about the total cost. If you carry dental insurance, you are likely wondering exactly how much of that investment your provider will cover and how much will come out of your own pocket.

At Royal Dental Care Schaumburg, we believe that navigating the maze of insurance should not be a frustrating mystery for our patients. While every policy is a unique legal contract between you, your employer, and your insurance provider, there are several general industry standards that apply to the vast majority of plans in the Schaumburg area. Gaining a deep understanding of how these “rules” function can help you plan your dental care with total confidence while avoiding unexpected bills.

A Deep Dive into the “Major Restorative” Category

In the complex world of dental insurance, procedures are typically categorized into three distinct “buckets” to determine how much the insurance company is willing to pay:

- Preventive Care: This includes routine cleanings, periodic exams, and standard X-rays. These are usually covered at 100% because insurance companies want to encourage you to avoid bigger problems.

- Basic Procedures: This typically covers small fillings, simple extractions, and sometimes deep cleanings for gum disease. These are often covered at 80%.

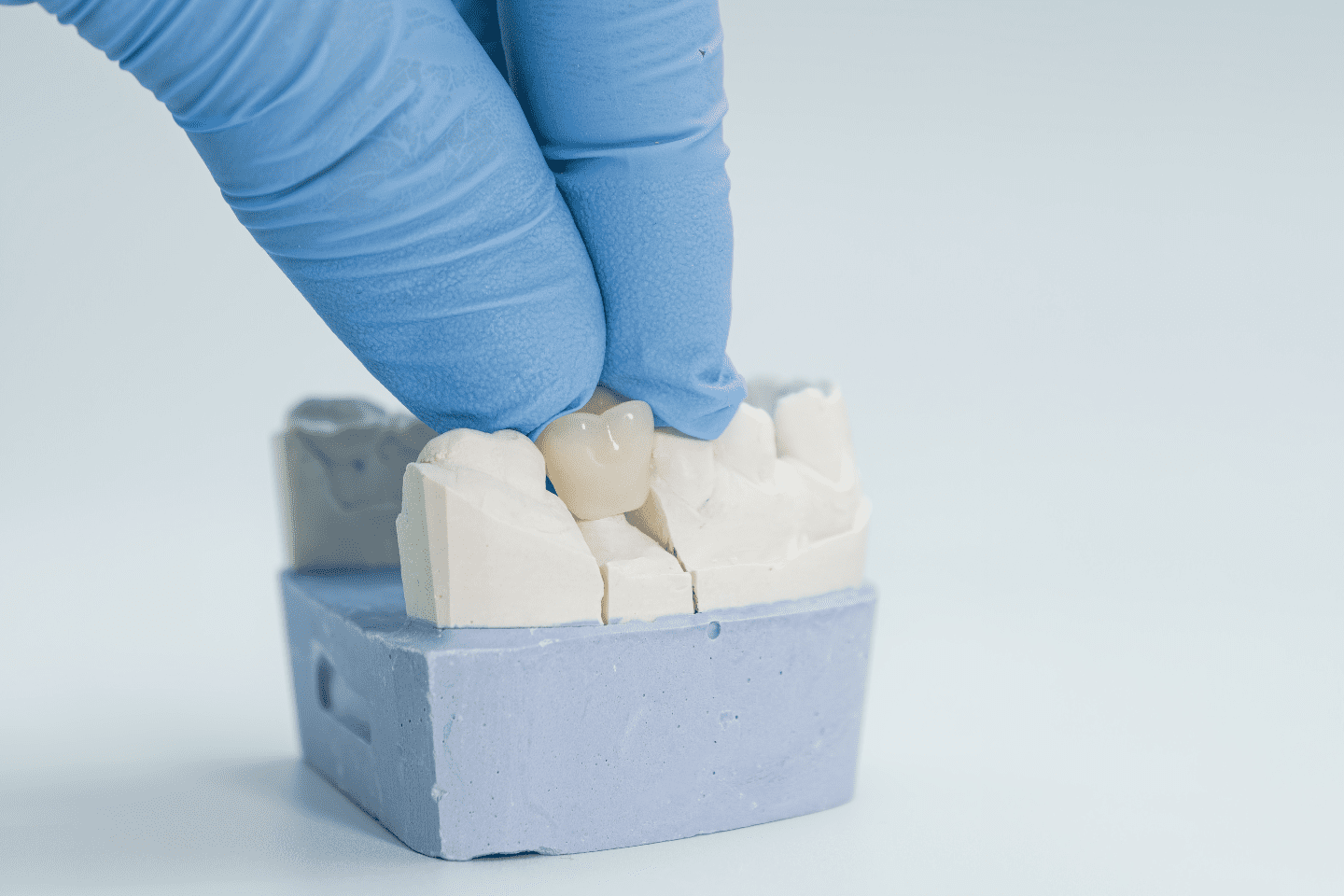

- Major Restorative Work: This is where dental crowns live. Because a crown involves high-level clinical skill, custom laboratory fabrication, and the use of high-quality materials like porcelain, ceramic, or zirconia, it is almost always classified as Major.

For most traditional dental plans used by residents in Schaumburg, Major Restorative work is covered at 50%. This means that once you have met your annual deductible (which is usually a small flat fee like $50 or $100), the insurance company typically pays half of their negotiated fee, and you are responsible for the remaining 50%. It is important to remember that this “negotiated fee” is a set price agreed upon by the dentist and the insurance company, which is often lower than the standard office price.

The Vital Role of “Clinical Necessity”

A common point of confusion for patients is why insurance might deny a claim for a crown that a dentist has recommended. Insurance companies generally only provide financial coverage for crowns when they are deemed “clinically necessary.” This means there must be objective, clear evidence showing that the tooth cannot be fixed with a simple filling.

When we submit a claim to your insurance provider, we include:

- High-Definition Intraoral Photos: These show the cracks, large old leaking fillings, or broken cusps that are visible to the naked eye.

- Digital X-rays: These allow the insurance adjuster to see decay that has worked its way deep into the tooth or under an old restoration.

- Clinical Narratives: Our doctors write detailed notes explaining why a crown is the only way to ensure the long-term survival of the tooth.

If you are looking to get a crown purely for cosmetic reasons—for instance, to hide a slight discoloration on a perfectly healthy tooth or to change the shape of a tooth you don’t like—the insurance company will likely categorize the treatment as “elective.” In these cases, they may not provide any coverage at all. At Royal Dental Care Schaumburg, we are very experienced in providing the rigorous documentation required to show why a crown is a vital medical necessity for your oral health.

Key Factors That Can Change Your Coverage

When you are searching for a dentist in Schaumburg, IL, it is incredibly helpful to have your insurance card or benefit booklet ready so the office can investigate the fine print of your specific plan. Here are several common clauses that can significantly impact your final out-of-pocket costs:

The Annual Maximum

Unlike medical insurance, which protects you against unlimited costs, dental insurance has a “cap” on what they will pay out in a single calendar year. This is usually between $1,000 and $2,000. If you have already had other dental work done earlier in the year such as several fillings or a root canal, you may have already used up a large portion of that maximum. If the 50% coverage for your crown exceeds your remaining balance for the year, you will be responsible for whatever the insurance company cannot pay.

Waiting Periods

This is a common hurdle for people who have recently started a new job or signed up for an individual insurance plan. Many companies implement a waiting period of 6 to 12 months before they will pay for “Major” work. This is designed to prevent people from signing up for insurance only when they know they need an expensive procedure. Our front desk team can help you check your plan’s effective date to see if a waiting period is still active.

The “Five-Year” or “Ten-Year” Rule

Insurance companies operate on the logic that a well-made crown should last a long time. Therefore, most policies will only pay for a replacement crown on the same tooth once every five to ten years. If you have a crown that failed prematurely—perhaps due to a new cavity forming underneath it—and it has only been three or four years since it was placed, the insurance company might deny the claim. In these situations, we have to work extra hard to prove that the failure was unavoidable and that the tooth is currently at risk.

The LEPAT Clause

LEPAT stands for “Least Expensive Professionally Acceptable Treatment.” This is a tricky clause where the insurance company will only pay for the cheapest version of a fix. For example, if you want a beautiful, metal-free porcelain crown that looks exactly like a natural tooth, but the insurance company decides a silver-colored metal crown is “acceptable,” they will only pay the amount for the metal crown. You would then be responsible for the price difference to get the porcelain one.

Strategic Financial Planning at Royal Dental Care

We understand that even with 50% insurance coverage, a high-quality dental crown represents a significant financial commitment. We never want the cost of care to be the reason a patient loses a tooth that could have been saved. If your insurance coverage is lower than you expected, or if you don’t have insurance at all, we offer several strategic ways to manage the cost:

- In-House Membership Plans: We have designed a special program for our patients without insurance. For a flat annual fee, you receive your cleanings and exams at no extra cost, plus a significant, guaranteed discount on restorative work like crowns. This often ends up being more cost-effective than a traditional insurance plan with high premiums and low maximums.

- Third-Party Financing: We work with reputable providers like CareCredit and Sunbit. These services allow you to break the total balance of your crown into monthly payments. Many of our patients qualify for 6-month or 12-month interest-free options, making the treatment fit easily into a monthly household budget.

- Treatment Phasing: If you have multiple teeth that need crowns, we don’t always have to do everything at once. We can prioritize the most urgent tooth and then schedule the next one for the following “insurance year.” By doing one crown in December and another in January, you can use two years’ worth of annual maximums to cover the work.

Frequently Asked Questions

Q: Do I need to get a “pre-approval” before my appointment?

A: While it isn’t legally required to start work, we strongly recommend a “Pre-Determination of Benefits.” We send the digital X-rays and the treatment plan to your insurance company before we ever pick up a drill. Within a few weeks, they send back a document stating exactly how much they estimate they will pay. This takes the stress and guesswork out of your final bill.

Q: Is the “build-up” under the crown covered?

A: Most of the time, a tooth is so damaged that we have to perform a “core build-up” first. This is a specialized, high-strength filling that creates a sturdy foundation for the crown to sit on. Insurance coverage for this is hit-or-miss; some plans bundle it with the crown, while others pay for it separately. We check this for you during the initial planning stage.

Q: Can I use my HSA or FSA funds?

A: Absolutely. Using your Health Savings Account or Flexible Spending Account is one of the smartest ways to pay for dental work. Because those funds are put aside pre-tax, you are essentially getting a 20% to 30% discount on your portion of the bill, depending on your tax bracket.

Our Commitment to Your Health and Budget

At Royal Dental Care Schaumburg, we know that talking about money and insurance can be the most stressful part of going to the dentist. Our administrative team is dedicated to being your personal advocate. We spend hours on the phone with insurance adjusters so that you don’t have to.

When you are looking for the best dentist in Schaumburg, IL, you want a team that provides world-class clinical results while also respecting your time and your hard-earned money. We promise to be completely upfront about all costs and to help you squeeze every bit of value out of your insurance benefits. Your dental health is our top priority, and we are here to help you find a way to make the best possible treatment a reality for your smile.

Do you have more questions about your specific dental plan or a tooth that’s been bothering you? Contact Royal Dental Care Schaumburg today. We are happy to perform a complimentary insurance verification and help you understand all your options for restoring your smile.

Real Patients. Real Reviews.

Luke

11 months ago

Isabella was great!! Highly recommend her

Julia Swider

11 months ago

Great experience, everyone is very kind and patient. Take time to educate you on what is going on, which is much appreciated. Highly recommend!

Response from the owner 1 year ago

Hi Julia,Thank you for leaving us a review! Your feedback is appreciated.

Pawel Blaszczak

11 months ago

Casey Kinsella

11 months ago

The atmosphere was great. The professionals were friendly. The communication between the office, dentist and patient was awful. I’ve found this with most dentist offices that once they get your money, they forget about you. Not happy with the customer service.

Scott Donaldson

11 months ago

Szymon Szuster

11 months ago

Ozzie Skenderi

11 months ago

Everyone is so nice and helpful!! They are great!!

Response from the owner 1 year ago

Hi Ozzie,We appreciate you taking the time to provide your feedback. We're happy to hear you had a positive experience at our practice!

Jacqueline Hernandez

11 months ago

Really clean and great service

Rafal Raszewski

11 months ago

vivian trankina (viv)

11 months ago

amazing service everyone is kind here i’ve been going here for about 2 ywars

Keluarga Bahagia

11 months ago

Since I moved from another dentist to this Royal Dental treatment has felt so amazing, all the women who work at the desk are very kind to help me and my husband for scheduling, especially for me a dental cleaner who cleans my teeth Lois is my favorite, she is very friendly and does clean details. The dentist is also good, twice helped by the dentist forgot his name, he is also very helpful to check, for all the good and happy come to this Kingdom's teeth

Karina Czajko

11 months ago

Very professional, always respectful! Highly recommend!

Yoly navarrete

11 months ago

The atmosphere is beautiful the place is very clean. Very professional service. I went in for a free consultation. They were very thorough at explaining everything. I will be coming back and I Recommend them.

Alyssa Silvia

11 months ago

Response from the owner 11 months ago

Hi Alyssa Silvia Thanks for visiting Royal Dental Care. We truly value your feedback and your confidence in our team.

Amreen Jalal

11 months ago

izabela was so sweet and made the entire appointment very easy and enjoyable. the environment was really friendly, welcoming and clean. would definitely recommend to others, they’re very thorough with their work!

Response from the owner 11 months ago

Hi Amreen Jalal Thanks for taking the time to leave a review. Your input helps us continue providing high-quality care at Royal Dental Care.

LUKASZ WROBLEWSKI

11 months ago

This is a great place for those who want a gentle dentist, a thorough hygienist, and friendly staff. Everyone is so nice, and the whole office is clean and modern.

Response from the owner 11 months ago

Hi LUKASZ WROBLEWSKI Thank you for your kind words. We're so pleased to know you had a great experience at Royal Dental Care.

Katherine Dynak

11 months ago

Pretty good service

Response from the owner 11 months ago

Hi Katherine Dynak Your feedback means a lot to our team. We're committed to continuing the excellent care you’ve come to expect.

Melissa

11 months ago

Very friendly staff. Professional, I’ve been coming here for years now

Response from the owner 11 months ago

Hi Melissa We appreciate your support and are grateful you chose Royal Dental Care for your dental needs. Looking forward to seeing you again.

Bobby Anderson

11 months ago

I love this place! Been coming for years. I’ve had a lot of work done lol

Response from the owner 11 months ago

Hi Bobby Anderson Thank you for your kind words. We're so pleased to know you had a great experience at Royal Dental Care.

Rosa Rendon

11 months ago

Very good experience, Israa was amazing and did a great job

Response from the owner 11 months ago

Hi Rosa Rendon Your feedback means a lot to our team. We're committed to continuing the excellent care you’ve come to expect.